Introduction

When small businesses need funding, two common options come to mind: Merchant Cash Advances (MCAs) and Business Loans. While both provide access to capital, they differ significantly in cost, repayment structure, and suitability for different business needs. Choosing the right option can make a big difference in your financial health. In this guide, we’ll compare merchant cash advances and business loans to help you make an informed decision.

What Is a Merchant Cash Advance (MCA)?

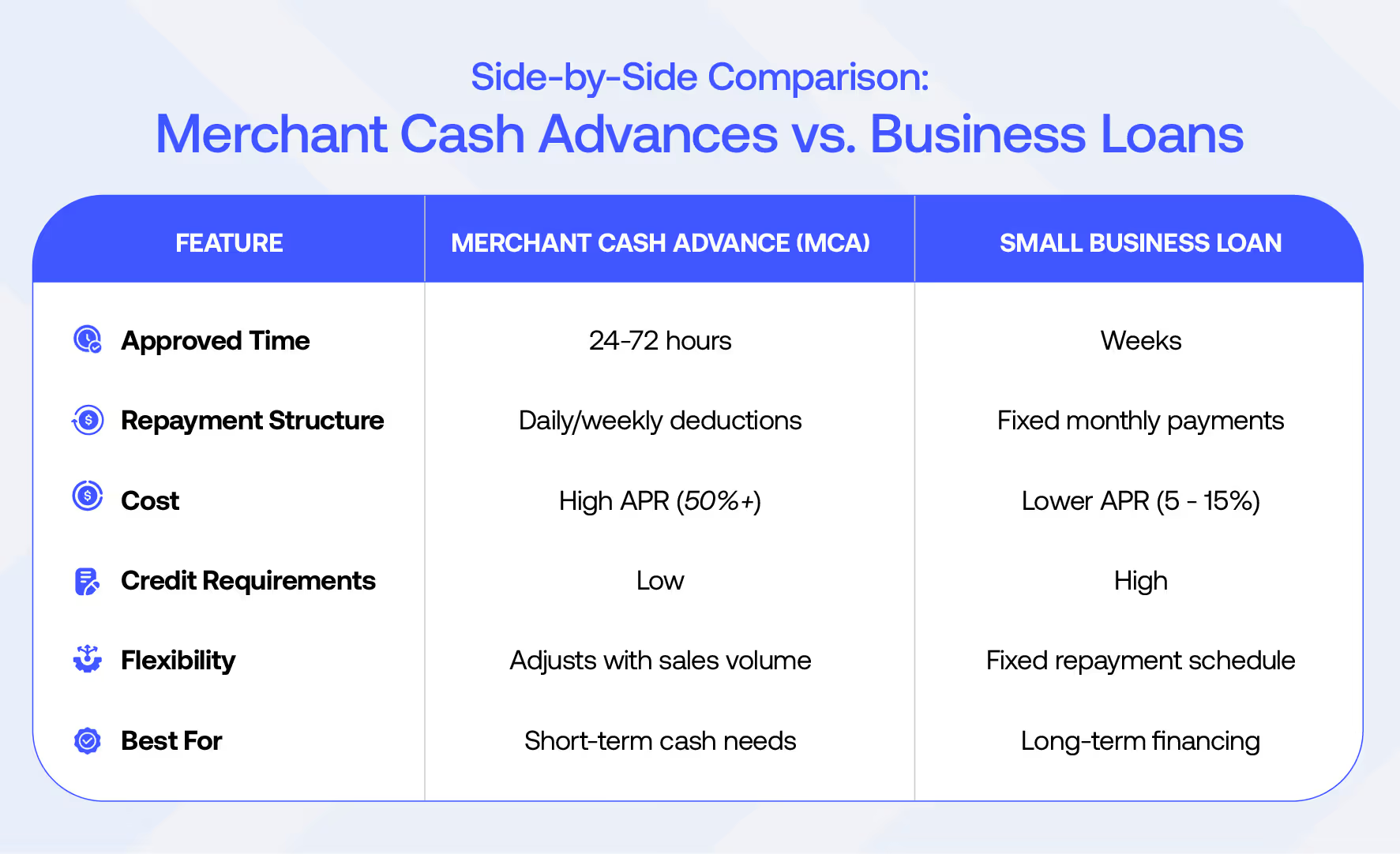

A Merchant Cash Advance is a lump sum of cash provided upfront in exchange for a percentage of your future sales. Unlike traditional loans, MCAs often feature revenue-based repayment structures that fluctuate based on your daily sales. Alternatively, some MCAs use fixed daily or weekly payment amounts, which remain constant regardless of sales performance.

Key Features of MCAs

- Repayment: Automatically deducted daily or weekly from credit/debit card sales.

- Cost: Uses a factor rate (e.g., 1.2 or 1.5) instead of an interest rate, often leading to APRs of 50% or more.

- Approval Process: Based on business revenue rather than credit score.

Pros of MCAs

- Fast approval and funding, often within 24–72 hours.

- Some MCAs offer flexible repayments that adjust with sales volume.

- No need for high credit scores or extensive documentation.

Cons of MCAs

- High repayment costs can strain cash flow.

- Lack of regulation compared to traditional loans.

- No benefits for early repayment—you owe the full factor amount.

What Is a Business Loan?

A Business Loan is a traditional financing option where lenders provide a lump sum that is repaid over time with interest. Loans can be secured (requiring collateral) or unsecured.

Key Features of Business Loans

- Repayment: Fixed monthly payments over a set term.

- Cost: Typically lower APRs than MCAs, often ranging from 5% to 15%.

- Approval Process: Requires strong credit and financial documentation.

Pros of Business Loans

- Lower borrowing costs compared to MCAs.

- Predictable repayment terms, making budgeting easier.

- Suitable for long-term financing needs like expansion or equipment purchase.

Cons of Business Loans

- Longer approval process, often taking weeks.

- Requires good credit history and detailed financial records.

- May require collateral for secured loans.

Side-by-Side Comparison: Merchant Cash Advances vs. Business Loans

When Should You Choose a Merchant Cash Advance?

MCAs are ideal if your business:

- Needs fast funding to cover immediate expenses, like payroll or inventory.

- Has steady credit card sales to support daily or weekly repayments.

- Cannot qualify for traditional loans due to poor credit or lack of collateral.

When Should You Choose a Business Loan?

Business loans are a better fit if your business:

- Has time to wait for the approval process.

- Needs lower-cost financing for long-term projects, like expansion or equipment purchases.

- Has a strong credit history and can provide required documentation.

Case Study: MCA vs. Business Loan in Action

Scenario 1: A Restaurant Owner Needs Emergency Repairs

- Solution: An MCA might be appropriate due to fast approval and funding.

Scenario 2: A Retailer Plans to Open a New Location

- Solution: A business loan is often the better choice, offering affordable financing with predictable terms for long-term growth.

The Risks of Choosing the Wrong Option

- With an MCA: High repayment costs and daily withdrawals can create a cash flow crunch, leaving businesses worse off than before.

- With a Business Loan: A lengthy approval process may delay funding, causing missed opportunities or financial strain in urgent situations.

How Coastal Debt Resolve Can Help

If your business is struggling with high-cost MCA debt, Coastal Debt Resolve offers solutions to help you regain control:

- Negotiate Lower Repayment Terms: Work with MCA providers to reduce repayment amounts.

- Debt Resolution Plans: Create manageable repayment schedules tailored to your cash flow.

- Restructuring Timelines: Extend repayment durations to lower monthly obligations and improve affordability.

Our team has helped hundreds of businesses break free from MCA debt and restore financial stability.

FAQs About MCAs and Business Loans

1. Are MCAs considered loans?

No, MCAs are advances on future sales, not loans. This distinction exempts them from certain lending regulations.

2. Can I refinance an MCA into a business loan?

Yes, in some circumstances refinancing into a lower-cost business loan may help reduce the financial burden of high-interest MCA repayments.

3. How do I calculate the cost of an MCA?

Multiply the advance amount by the factor rate to determine the total repayment amount. For example, a $10,000 advance with a 1.4 factor rate requires $14,000 in repayment.

Conclusion

Choosing between a Merchant Cash Advance and a Business Loan depends on your business’s financial needs, urgency, and repayment capacity. While MCAs offer fast funding, their high costs make them a short-term solution. Business loans, on the other hand, provide affordable financing but require more time and stronger credit. If you’re struggling with MCA debt or need guidance regarding the best financing option, Coastal Debt Resolve is here to help.

Call to Action

Need help navigating your business financing options or escaping the MCA debt cycle? Contact Coastal Debt Resolve today for expert advice and customized solutions.

Disclaimer: The information provided in these materials is for general informational purposes only and is not intended as legal, tax, or financial advice. While we strive to ensure that the content is accurate and up-to-date, it should not be relied upon as a substitute for legal advice.

Frequently asked questions

If a significant portion of your revenue is going toward debt repayments, or if you’re taking out new loans to cover old ones, you may be in a debt cycle.

Track your income and expenses carefully, speed up receivables, and reduce unnecessary costs to maintain positive cash flow.

While not always necessary, an accountant can provide invaluable insights into tax planning, financial management, and long-term growth strategies.