Introduction

Merchant Cash Advances (MCAs) are often marketed as fast, flexible funding solutions for small businesses in need of immediate cash flow. While they provide quick access to capital, the true cost of an MCA can be much higher than it initially appears. Unlike traditional loans with straightforward interest rates and repayment terms, MCAs use factor rates, daily deductions, and hidden fees that can make them one of the most expensive financing options available.

In this article, we’ll break down the real cost of MCAs, explain how to calculate their financial impact, and explore alternative solutions to help your business avoid debt traps.

How Merchant Cash Advances Work

Unlike traditional loans, MCAs are not loans—they are cash advances based on a business’s future sales. The lender provides a lump sum upfront, and the business repays the advance through daily or weekly deductions from its sales.

Key Features of an MCA

- Fast Approval: Businesses can receive funding in as little as 24-72 hours.

- No Fixed Payments: Repayments fluctuate with daily sales.

- No Collateral Required: Most MCAs are unsecured, meaning no business assets are listed as collateral.

- High Costs: The real cost of borrowing can be significantly higher than traditional financing.

The True Cost of Merchant Cash Advances

Many business owners don’t realize how expensive MCAs are until they are locked into a repayment cycle. Below are the biggest cost factors to consider.

1. The Factor Rate – A Hidden Interest Cost

Instead of using an Annual Percentage Rate (APR) like traditional loans, MCAs use a factor rate, which is a fixed multiplier applied to the loan amount.

- Factor rates typically range from 1.2 to 1.5

- Unlike interest rates, the factor rate does not decrease over time

- You owe the full amount upfront, regardless of how quickly you repay

Example Calculation:

A business takes a $20,000 MCA with a 1.4 factor rate. This means the total repayment amount is:

$20,000 × 1.4 = $28,000

This means the business must repay $8,000 more than the amount borrowed, even if they pay it back early.

Compare to a Traditional Loan:

A $20,000 bank loan at a 10% APR over 12 months would cost around $2,000 in interest, far less than an MCA.

2. Frequent Repayments Strain Cash Flow

Unlike traditional loans with monthly payments, MCAs require daily or weekly deductions from sales.

- MCA providers typically take 10%-20% of daily sales

- This can drain cash flow and leave businesses struggling to cover operational costs

- Payments continue until the full balance (factor rate included) is paid off

Example:

A restaurant with $2,000 in daily sales and a 15% MCA repayment rate would have $300 deducted every day.

Problem: What happens if business slows down? Even if sales drop, MCA payments continue, leading to financial strain.

3. Effective Interest Rates Can Exceed 100%

While MCA providers advertise factor rates, they don’t disclose the true APR. Because MCAs are repaid quickly (often within 6-12 months), the effective APR can be much higher than traditional loans.

Example of True Cost:

A $20,000 MCA with a 1.4 factor rate (total cost = $28,000) repaid in 5 months has an effective APR of over 100%.

Comparison:

A business loan with a 10% APR over 5 years would have an effective cost far lower than an MCA.

The Hidden Dangers of MCAs

Merchant Cash Advances aren’t just expensive—they can also trap businesses in cycles of debt.

- Debt Stacking: Many businesses take multiple MCAs to cover previous ones, leading to unsustainable debt.

- No Benefit to Early Repayment: Unlike loans, MCAs charge the full factor rate regardless of when you pay it off.

- Limited Business Growth: High daily repayments leave businesses without working capital to reinvest.

How to Avoid the MCA Debt Trap

If your business is struggling with MCA payments, here are a few strategies to regain financial stability.

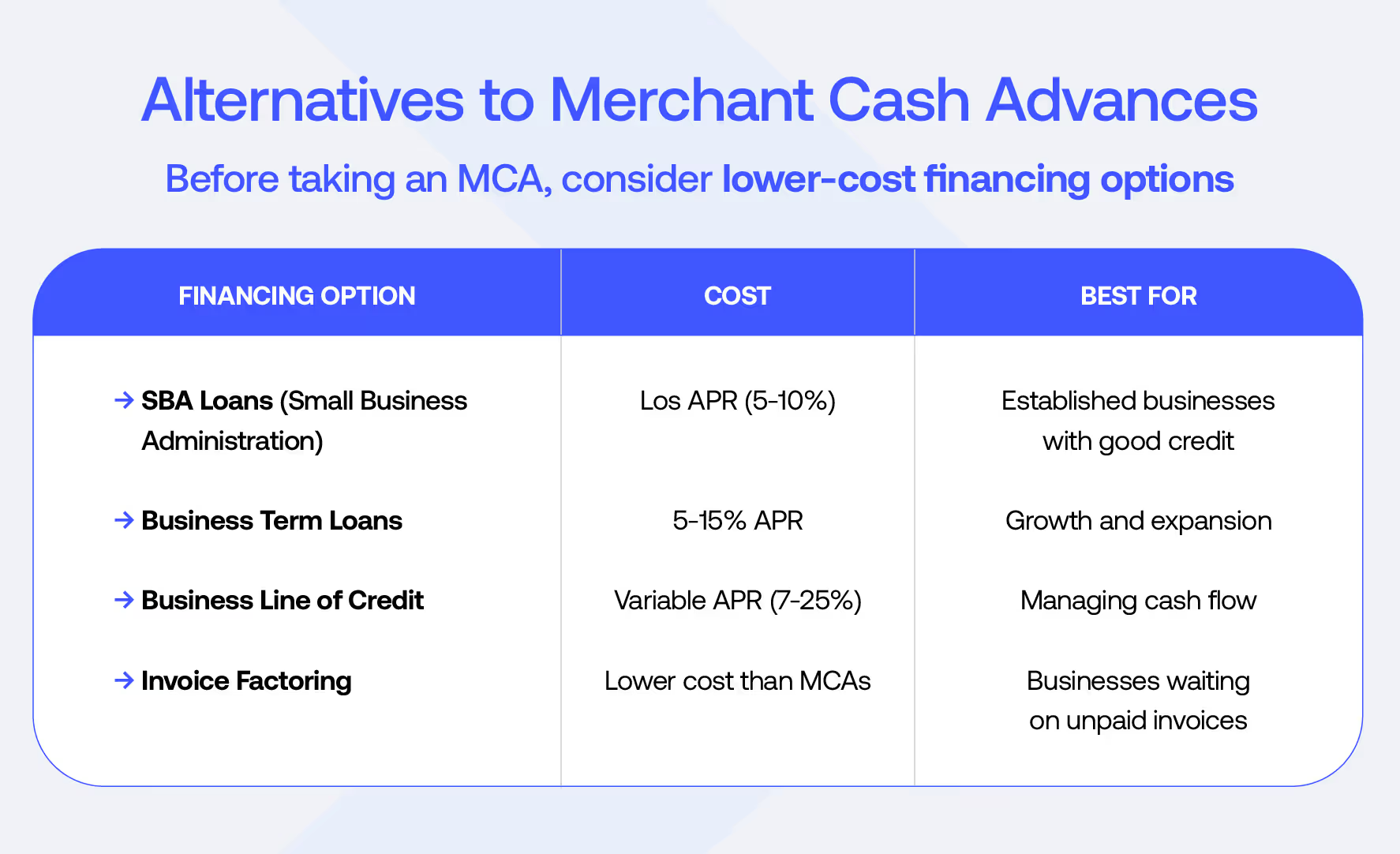

1. Refinance MCA Debt

- Business Term Loans: Convert expensive MCA debt into a lower-cost term loan.

- Business Line of Credit: A revolving line of credit provides flexible funding at lower interest rates.

2. Negotiate with MCA Providers

- Some MCA companies may agree to modify repayment terms to ease financial strain.

3. Work with a Debt Resolution Specialist

Coastal Debt Resolve specializes in helping businesses escape high-cost MCA debt. Our team can:

- Negotiate settlements to reduce the total repayment amount.

- Structure a payment plan that aligns with cash flow.

- Protect your business from legal risks and aggressive collection tactics.

Alternatives to Merchant Cash Advances

Conclusion

Merchant Cash Advances may offer quick cash, but their true cost is much higher than it seems. With high factor rates, frequent repayments, and no early repayment benefits, many businesses find themselves trapped in debt cycles.

Before taking an MCA, explore lower-cost alternatives like business loans, lines of credit, or invoice factoring. If you’re already struggling with MCA debt, Coastal Debt Resolve can help you negotiate better terms, reduce your repayment burden, and regain financial stability.

Call to Action

Is your business struggling with MCA debt? Coastal Debt Resolve can help. Contact us today for a free consultation and take the first step toward financial relief.

Disclaimer

The information provided in these materials is for general informational purposes only and is not intended as legal or financial advice. While we strive to ensure that the content is accurate and up-to-date, it should not be relied upon as a substitute for legal advice. Performance information may have changed since the time of publication. Past performance is not indicative of future results.

Frequently asked questions

Multiply the advance amount by the factor rate (e.g., $20,000 × 1.4 = $28,000).

No. MCA providers charge the full factor rate, meaning there is no savings for early repayment.

Contact a debt resolution service like Coastal Debt Resolve to explore restructuring or settlement options.